Custodian Controlled

Self-Directed IRA

Self-Directed IRA

Self-Directed IRA LLC with

Checkbook Control

Checkbook Control

24,000+ clients

Our tax and ERISA experts have helped over 24,000 clients in all 50 states.

No hidden fees

No transaction or asset value fees. No minimum balance requirement (with credit card on file).

Serve as your custodian

Holds over $3.2 Billion in alternative assets.

Expertise

IRA Financial’s founder, Adam Bergman, is the author of nine books on self-directed retirement.

Dedicated support

Get direct access to a self-directed retirement expert to establish your plan.

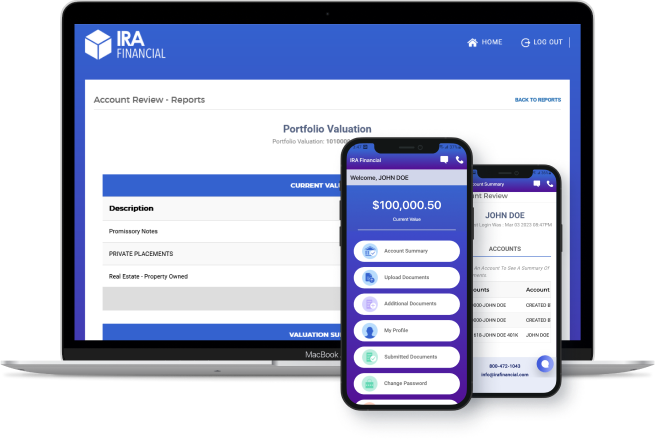

Technology

Use our app to set up and maintain your account.

Complete your application

Once completed, it will go into a queue to be reviewed (generally, 3-5 days).

Application is reviewed

Your application is reviewed to ensure everything is filled out correctly

Account number assigned

Once your application is approved, an account number is assigned and emailed to you (an additional 3-5 days).

Fund your account

You can now fund your Self-Directed IRA via transfer, rollover, or direct contribution.

Start investing

Once your IRA is funded, you can begin making investments!